Demonetization is a big opportunity for India to reach $10-trillion economy by 2030, thanks to sustained double-digit growth for the next 14 years as presently a large percentage of money will transact to the banking and digital system

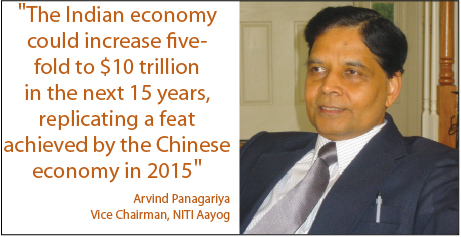

“India started off to rapid growth a little later than China, but now it has the potential to accomplish in the next 15 years what China did in the last 15 years. India’s GDP stands at $2 trillion and it has good prospects of rising to $10 trillion in the next 15 years," commented Panagariya.

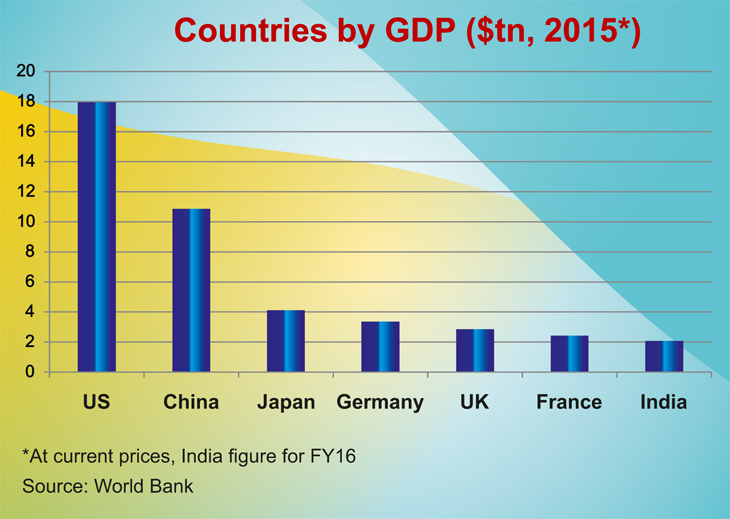

With $10.86 trillion (14.7 per cent share in the world GDP), the Chinese economy stood second in the world after the US in 2015 at $17.95 trillion, while India, at $2.07 trillion (2.8 per cent), was ranked seventh. Analysts reckon that to reach $10 trillion, the Indian economy needs to grow at over 11 per cent for the next one-and-a-half decades, which is a daunting challenge but not impossible as China’s economy was $1.2 trillion in 2000.

Prime minister’s Narendra Modi’s November 8 announcement of discontinuing Rs.500 and Rs.1,000 notes has given a big fillip to India achieving $10-trillion economy as diemonetization of Rs.500 and Rs.1,000 bank notes will definitely help India with a faster GDP growth, help in bringing down inflation and products becoming more affordable which will fuel the demand and further growth of the industries

Demonetization is not the final destination. It is just a beginning, said Prime Minister Narendra, while addressing the BJP parliamentary meeting on the last day of the winter session of Parliament.

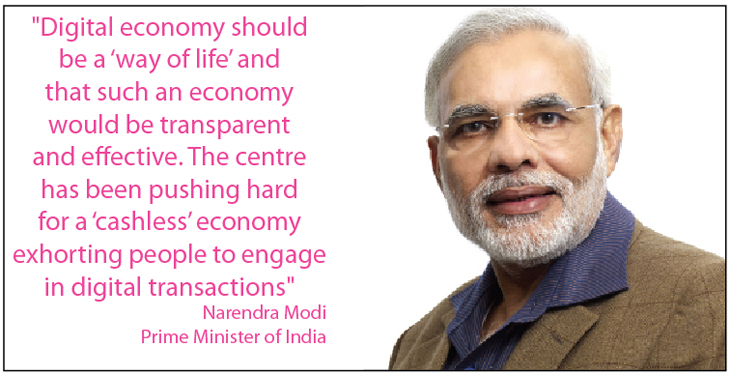

Addressing law-makers, Shri Narendra Modi said that a digital economy should be a “way of life” and that such an economy would be transparent and effective. The centre has been pushing hard for a “cashless” economy exhorting people to engage in digital transactions.

This one announcement has given a big jump to the Digital Payment industry in India. The BCG-Google Digital Payment Report 2020 forecasts total payments conducted via digital payment instruments in India will be in the range of $500 billion by 2020, which is approximately 10x of the current levels.

According to the report, Person to Merchant (P2M) transactions driven by digital payments at physical point of sale, followed by business to business (B2B) and peer to peer (P2P) transactions are expected to be major contributors of growth. Digitization of cash will accelerate over the next five years with non-cash transactions overtaking cash by 2023.

Mobile-based payment solutions and proprietary payment networks will drive merchant acquisition by offering low-investment solutions that will make economics more attractive for merchants and acquirers, resulting in over 10 million merchant establishments that will accept digital/mobile payments.

Modified Unified Payments Interface (UPI) will be a game-changer as it provides a great platform for seamless interoperability of PSPs. Modified to overcome the present challenges, it can drive large-scale adoption of digital payments.

Non-cash payment transactions which, today, constitute 22 per cent of all consumer payments will overtake cash transactions by 2023. Digital payments instruments will drive the growth in non-cash payments. Not only the BCG-Google report, even the GSMA report talks about the increased role of mobile in digital payments. The GSMA report “The Mobile Economy: India 2016” noted at the end of June 2016, 616 million unique users had subscribed to mobile services in India, making it the second-largest mobile market globally, with almost one billion unique mobile subscribers expected by 2020. India also overtook the United States in 2016 to become the world’s second- largest smartphone market with an installed base of 275 million mobile devices.

The report forecasts 4G subscribers to reach 280 million by 2020 and operators capex investment growing to $34 billion over 2016-2020 period. As per GSMA, the India mobile economy is more than $140 billion (Rs.9 lakh crore) and it is expected to grow to $210 billion (Rs.14 lakh crore) by 2020.

Speaking on digital payments, Pradeep Sampath, COO, mRUPEE (a subsidiary of Tata Teleservices), said, “The digital payments industry today is worth a staggering $9-trillion figure. With home to 1.25 billion people, India will still take time to go completely digital. As on date, payment revenues in India account for nearly $14 billion. However, the recent wave of demonetization is changing the shape of the digital payment industry.”Talking about the mobile economy, Mats Granryd, Director General, GSMA, said, “With The Mobile Economy: India 2016 report, all signs lead to a period of tremendous growth for India’s mobile economy, which will strongly support and enable the government’s Digital India initiative aimed at providing broadband connectivity to all.”

Speaking on digital payments, Pradeep Sampath, COO, mRUPEE (a subsidiary of Tata Teleservices), said, “The digital payments industry today is worth a staggering $9-trillion figure. With home to 1.25 billion people, India will still take time to go completely digital. As on date, payment revenues in India account for nearly $14 billion. However, the recent wave of demonetization is changing the shape of the digital payment industry.”Talking about the mobile economy, Mats Granryd, Director General, GSMA, said, “With The Mobile Economy: India 2016 report, all signs lead to a period of tremendous growth for India’s mobile economy, which will strongly support and enable the government’s Digital India initiative aimed at providing broadband connectivity to all.”

Commenting on UPI apps, Chinmay Agarwal, CTO & Co-Founder, Jugnoo, said, “On the mobile phone front, common minimum guidelines for UPI apps need to be defined so that user interface has a minimum common workflow. UPI distinctions for Peer to Merchant (P2M) and Peer to Peer (P2P) payments are confusing. P2P is simpler and should be promoted more. Further, we need to quickly release UPI SDKs for iOS and web platforms.”

“One of the key obstacles is trust and availability of mobile payment models – be it UPI or wallets to be available widely for transactions. The penetration is still too low for the population size of India, which transacts using cash. Even credit card or debit card penetration has not been very successful in doing cashless transaction for lack of basic infrastructure,” says Govind Ramamurthy, CEO & MD, eScan.

Even demand for Point of Sale (PoS) devices is huge for cashless transactions, both for making payments or disbursing cash. So the Government has exempted it from excise duty, and consequently from CVD and SAD and it is valid till March 31, 2017.

Digital Payment Options

|

As on November 30, 2016, RBI gave approval to 195 banks for providing mobile banking services to their customers. Further, to facilitate mobile banking, the process of registration has been made convenient by enabling such feature on ATMs.

National Payments Corporation of India (NPCI) has offered the facility of mobile banking using Unstructured Supplementary Service Data (USSD) based mobile banking. USSD-based mobile banking offers basic banking facilities like money transfer, bill payments, balance enquiries, merchant payments, etc on a simple GSM mobile phone, without the need to download application on a phone, as required at present in the IMPS (Immediate Payment Service) based mobile banking.

Transactions can be performed on basic feature phone handsets. The user needs to approach his bank and get his mobile number registered. The bank will issue an MPIN (Mobile PIN) to the user. The user thereafter needs to dial *99# and the menu for using USSD opens. Thereafter customer has to follow selections on the menu to complete the transaction.

Speaking on USSD, Aruna Sundarajan, Secretary, MeitY, said, “Banks should work towards making USSD a preferable and convenient mode of digital payments in the light of the fact that majority of Jan Dhan account holders would directly benefit from it.”

NPCI will soon launch a redesigned USSD platform and a common app for UPI for enabling digital transactions, as well as addressing interoperability issues.

Mobile Wallet business is picking up with demonetization announcement – be it Paytm, MobiKwik, Oxigen, Freecharge and others. Recently, the Paytm Android app crossed the 50 million installs landmark on Google Play Store. With this, the Paytm's Android base has now grown to over 75 million.

L. V. Sastry, Vice-President – Mobile Banking & Commerce, Aircel, said, “Indian wallet transactions over the last three years by value and volume have grown by over 500 per cent to reach $551 million and 2.6 billion, respectively in 2015. In India, nearly 95 per cent of all the transactions are cash based, signalling a huge opportunity and upside to this growing usage of mobile phones for financial transactions.”

Currently, there are over 200+ million active mobile wallets with over 75 million transactions every month and payment throughput of over Rs.2,000+ crore of payments is being processed across the country.

Paytm has set a target of 200 million accounts which will include current and savings accounts as well as mobile wallets within 12 months. The company also aims to reach a base of half a billion accounts by the year 2020. The company has also announced that it would transfer its wallet business to the newly incorporated Paytm Payments Bank after receiving necessary approvals. Paytm claims to have close-to 155 million e-wallet users, which include users on the web and smartphone apps.

On the merchant front, Paytm expects to onboard 500,000 merchants on its platform to accept offline payments as the country grapples with a shortage of cash due to the Narendra Modi demonetization move.

To enable millions of feature phone users to go digital, Paytm has launched a service with which consumers and merchants can pay and receive money without internet connection. The company has announced a toll-free number 1800 1800 1234 to enable consumers and merchants without an internet connection to pay and receive money instantly and also recharge their mobile phones.

MobiKwik is another Indian wallet major with a network of over 250,000 direct merchants and 40 million-plus users. Founded in 2009 by Bipin Preet Singh and Upasana Taku, the company has raised three rounds of funding from Sequoia Capital, American Express, Tree Line Asia, MediaTek, GMO Payment Gateway, Cisco Investments and Net1.

Indian mobile wallet major, MobiKwik recently announced the launch of MobiKwik “Lite”, India’s lightest mobile wallet, to cash on demonetization bandwagon and help unorganized retailers and shopkeepers across India in receiving payments seamlessly.

MobiKwik Lite is an under 1 MB app that works smoothly on EDGE connections and slow data connectivity. Users can download this app with just one missed call at 8097180971 and sign up with their mobile number only,

Speaking on the launch, Bipin Preet Singh, Co-Founder, MobiKwik, said, “MobiKwik Lite will be available in all the major Indian languages soon. MobiKwik Lite will work without any net connectivity too, therefore addressing all the challenges being faced by the masses in accessing wallet payments – be it language, connectivity or quality of smartphones.”

Oxigen has a retail footprint of 200,000 outlets and has processed over 2 billion transactions till date with a current transaction volume rate of 600 million transactions per annum. It has a large customer base of over 150 million.

Oxigen Wallet is India’s first non-bank mobile wallet app approved by RBI, which allows users to send and receive money through popular social channels like Facebook, WhatsApp, Twitter, SMS and e-mail. A customer can instantly send money to any mobile number or bank account in India, even if the recipient is not a registered Oxigen Wallet user.

Oxigen Wallet claims to have 30 million users and is accepted at over 9,000 merchant locations and 10,000 online sites like Bookmyshow, ebay, PVR, OYO Rooms, Jabong, and more. Oxigen Wallet offers a safe, secure and convenient payment solution via the mobile.

Loading money into Oxigen wallet app is easy. One can use credit card, debit card or pay cash over the counter through any of Oxigen’s 200,000 retailer/ partners across the country. In 2016, Oxigen Services introduced its Micro ATM. Oxigen MicroATM provides Aadhaar biometric-based transactions for financial services.

Ankur Saxena, CEO, Oxigen Wallet, said, “In terms of transaction value, the company is planning to reach Rs.14,500 crore in FY 2016-17 in comparison to Rs.10,500 crore in FY 2015-16.”

Speaking about security, Ankur said, “Oxigen application is pretty secure. Once you log onto it is bound into one device. The transaction is all encrypted so security is no concern at the application end. Even when the phone is stolen, it does not make much of a difference as money is in cloud.”

Bharti Airtel through Airtel Payments Bank has rolled out its pilot services in Rajasthan, Andhra Pradesh, Telangana and Karnataka. Airtel has done a pilot rollout in Rajasthan, where over 100,000 customers opened savings accounts in less than two weeks of the commencement of services. In Andhra Pradesh and Telangana, Airtel Payments Bank is rolling out pilot services across 8,000 Airtel retail outlets in Andhra Pradesh and 7,000 outlets in Telangana, which also act as banking points. In Karnataka, Airtel Payments Bank is rolling out pilot services across 12,000 Airtel retail outlets. Airtel is planning 70 per cent of these banking points in rural areas, thereby driving financial inclusion and reaching unbanked/underbanked areas.In the age of demonetization, mobile operators like Bharti Airtel, Idea Cellular, Reliance Jio, Tata Teleservices and Vodafone are all banking a lot on mobile payments in a big way. All these operators are targeting consumers as well as merchants in an aggressive way to increase their share from mobile payment.

Bharti Airtel through Airtel Payments Bank has rolled out its pilot services in Rajasthan, Andhra Pradesh, Telangana and Karnataka. Airtel has done a pilot rollout in Rajasthan, where over 100,000 customers opened savings accounts in less than two weeks of the commencement of services. In Andhra Pradesh and Telangana, Airtel Payments Bank is rolling out pilot services across 8,000 Airtel retail outlets in Andhra Pradesh and 7,000 outlets in Telangana, which also act as banking points. In Karnataka, Airtel Payments Bank is rolling out pilot services across 12,000 Airtel retail outlets. Airtel is planning 70 per cent of these banking points in rural areas, thereby driving financial inclusion and reaching unbanked/underbanked areas.In the age of demonetization, mobile operators like Bharti Airtel, Idea Cellular, Reliance Jio, Tata Teleservices and Vodafone are all banking a lot on mobile payments in a big way. All these operators are targeting consumers as well as merchants in an aggressive way to increase their share from mobile payment.

Customers will now be able to open bank accounts at any of the designated Airtel retail outlets and enjoy a host of convenient banking services. As a special offer, customers opening a savings account with Airtel Payments Bank will also get one minute of Airtel mobile talk-time for every Rupee deposited. For example, if a customer opens an account with a deposit of Rs.500, then he/she will get 500 minutes of free talk-time for calls to anywhere in India on his/her Airtel mobile number.

Shashi Arora, MD & CEO, Airtel Payments Bank, said, “We are pleased to roll out our pilot services in Andhra Pradesh and Telangana and look forward to serving customers and contributing the financial inclusion vision of the two states. We have received an extremely positive response from customers in Rajasthan and would like to replicate the same in Andhra Pradesh and Telangana before we rollout our services nationally.”

Airtel Payments Bank is a fully digital and paperless bank and customers can access services over their mobile phones, including all feature/basic mobile phones. Airtel will leverage its vast customer base of over 260 million customers and educate them on the benefits of digital payments.

Airtel Payments Bank plans to develop a nationwide merchant ecosystem of over 3 million partners that will include small kirana stores, small shops and restaurants, etc.

Reliance Jio Money is also planning an aggressive pitch and is planning to sign over 10 million small merchant retailers in the coming weeks across 17,000 towns and 4 lakh villages.

|

To enable digital transactions, Reliance Jio is working to empower Indian merchants by building a digital retail ecosystem, called Jio Money Merchant Solutions. This will enable digital transactions of all types – be it at mandis, small shops, restaurants, railway ticket counters for bus and mass transit and even for person-to-person money transfers.

Starting December 5, every merchant can download Jio Money Merchant Solutions, whereas customers can use their Jio Money wallets to pay merchants from their bank accounts, and merchants can use the Jio Money Merchant app to accept these payments directly into their bank accounts.

Using Jio Money Merchant App, merchants can also make supplier payments, transfer money between his bank account and use digital petty cash.

The Jio Money ecosystem will be a committed and enthusiastic partner for the smooth implementation of Prime Minister Narendra Modi's game-changing vision of creating a digitally- enabled and a strong Indian economy.

Jio is committed to support the growth of a digitally-enabled, optimal-cash economy in India. In order to make this possible, JioMoney is rapidly expanding its reach to millions of touch points where Aadhaar-based micro-ATMs will be deployed.

mRUPEE, a subsidiary of Tata Teleservices, is a semi-closed wallet that is licensed by the RBI for offering customized solutions to corporates for simplifying employee payments and other processes. mRUPEE will be available as a payment option across all HPCL outlets, whereby the customers can make payments through mRUPEE. The company is also partnering with Intex, a leading mobile phone vendor, to launch “Intex MyWallet” app for its customers. Earlier this year, the company had tied up with IRCTC to provide a payment gateway, allowing users one-tap payments for rail ticket bookings.

|

The company has also tied up with ICICI Bank to launch a recharge facility for Delhi Metro cards. MMPL also launched the open loop prepaid, VISA-powered card in partnership with RBL Bank (Ratnakar Bank). By obtaining a PaySmart card, mRUPEE customers can withdraw money from VISA licensed ATMs and pay for goods and services at all merchants that accept VISA debit/credit cards nationally.

According to Vishal Gupta, Co-founder and CEO, Seclore Demonetisation will increase digitization; making information fluid and easily shareable with the right parties. Free movement of data oils the wheels of the modern enterprise – as well as the modern government. Improved productivity and better delivery of services are quick and provide immediate benefits however, the other key aspect of demonetisation is keeping track of all digital data across organisations, offices, networks, servers, devices and all other things – impossible with traditional security solutions. Traditional security solutions cannot deliver data-centric security and auditing of the entire digital cash trail. This is only possible with the data-centric security solutions like EDRM offered by Seclore.

Vodafone India has announced the launch of Vodafone M-Pesa PAY, an easy and ready-to-use digital payment solution to enable merchants and retailers to receive payments from their customers without any exchange of cash.

To start using this digital payment solution, retailers and merchants simply have to download Vodafone M-Pesa app and register for Vodafone M-Pesa PAY as a merchant. Once registered, they can notify an individual customer to make the payment due. Customers just need to click on the notification and make payment digitally using their M-Pesa wallet, bank account and debit or credit card.

Launching Vodafone M-Pesa PAY, Sunil Sood, MD & CEO, Vodafone India, said, “We started our journey towards enabling financial and digital inclusion in 2013 with the launch of Vodafone M-Pesa and have since made considerable progress by successfully establishing a franchise of over 8.4 million customers and nearly 130,000 outlets across the country. With the launch of Vodafone M-Pesa PAY, we are accelerating this journey by creating a platform for merchants and retailers to easily embrace digital payments and also encourage their millions of customers to pay via digital currency.”

All the mobile operators need to undertake a cross-country drive to educate and onboard retailers, merchants and consumers to start using mobile wallets as the preferred solution for receiving and making payments.

Digital Payment Promotions

|

The government petroleum PSUs/oil marketing government companies were asked by the Government to give incentive by offering a discount at the rate of 0.75 per cent of the sale price to consumers on the purchase of petrol/diesel if payment is made through a digital mode.

The government and RBI have taken various steps to bring down the cost of digital transactions. The MDR charges have been brought down significantly in the case of transactions up to Rs.2,000 made through debit cards, i.e. 0.25 per cent in the case of transactions below Rs.1,000 and 0.50 per cent in the case of transactions between Rs.1,000 to Rs.2,000.

With a view to promoting digital transactions and encouraging merchant establishments to accept such card payments, the Government has waived service tax on such amount charged while making payments though credit card, debit card, charge card or any other payment card. However, this waiver is limited to payments up to Rs.2,000 in a single transaction.

To expand digital payment infrastructure in rural areas, the Central Government, through NABARD, will extend financial support to eligible banks for deployment of 2 PoS devices each in 1 lakh villages with a population of less than 10,000. These PoS machines are intended to be deployed at primary cooperative societies/milk societies/agricultural input dealers to facilitate agri-related transactions through digital means. This will benefit farmers of one lakh villages, covering a total population of nearly 75 crore who will have the facility to do cashless transaction in their villages for their agri needs.

Railways, through their suburban railway network, will provide incentives by way of discount up to 0.5 per cent to customers for monthly or seasonal tickets from January 1, 2017, if payment is made through digital means. All railway passengers buying online ticket shall be given free accidental insurance cover of up to Rs.10 lakh.

Public sector insurance companies will provide incentive by way of discount or credit, up to 10 per cent of the premium in general insurance policies and 8% in new life policies of Life Insurance Corporation (LIC) sold through the customer portals, in case the payment is made through digital means.

Public sector banks are advised that merchants should not be required to pay more than Rs.100 per month as monthly rental for PoS terminals/Micro ATMs/mobile PoS from the merchants to bring small merchants on board the digital payment ecosystem.

For the payment of toll at toll plazas on National Highways using RFID cards/Fast Tags, a discount of 10 per cent will be made available to users in the year 2016-17.

|

To promote digital payment transaction in rural and urban areas, the Ministry of Electronics and IT (MeitY) has launched DigiShala to inform, educate and enable 2 crore citizens in the country to make digital transactions.

MeitY has launched DigiShala, a free to air channel which will impart information and education, especially in rural and semi-urban areas relating to Digital Payment ecosystem, its tools, benefit and processes. The channel will be available without any subscription fee and hence will be affordable to poor people.

To realize this objective, the Government has also conceptualized a campaign, “Digi Dhan Abhiyan” to enable every citizen, small trader and merchant to adopt digital payments in their everyday financial transactions. During the campaign, citizens as well as small merchants will be informed about various modes of digital payments by educating them to download, install and transact for various modes of digital payments.

On Digishala, citizens will be informed and educated about various digital payment options through step-by-step demos of making digital payments using UPI, USSD, Aadhaar-enabled payment systems, e-Wallets, Cards, etc, along with talk shows and panel discussions with experts.

Speaking about free DTH channel, Shri Ravi Shankar Prasad, Minister of Electronics and IT and Law & Justice, said, "DigiShala will enable and empower every citizen of the country, especially farmers, students, Dalits and women in rural areas to learn the usefulness and benefits of digital payment in our everyday life and to adopt the same on a mass scale.”

Apart from electronic channel, MeitY is also organizing DigiDhan Mela at the Major Dhyanchand National Stadium, Delhi. The event aims to handhold users in downloading, installing and using various digital payment systems for carrying out digital transactions. MeitY is also working with the MInistry of Urban Development and CSCs to organize DigiDhan Mela at smaller towns, cities and villages.

|

DigiDhan Mela will witness participation from banks, telecom companies, mobile wallet operators, transportation network companies, Aadhaar-enabled payment system (AEPS) vendors, Department of Post, merchants (through marketing associations), cooperatives like Kendriya Bhandars and organized retail fruits and vegetable chains like Safal, milk booths, Agricultural Produce Marketing Committees, etc.

Even NITI Aayog has launched incentive schemes Lucky Grahak Yojana and the Digi-Dhan Vyapar Yojana to give cash awards to consumers and merchants who utilize digital payment instruments for personal consumption expenditures. The scheme specially focusses on bringing the poor, lower middle class and small businesses into the digital payment fold. The scheme will become operational with the first draw on December 25, 2016 leading up to a mega draw on Babasaheb Ambedkar Jayanti on April 14, 2017. The scheme consists of two major components – one for consumers and the other for merchants.

In Lucky Grahak Yojana for consumers, there is a daily reward of Rs.1,000 to be given to 15,000 lucky consumers for a period of 100 days and weekly prizes worth Rs.1 lakh, Rs.10,000 and Rs.5,000 for consumers who use the alternate modes of digital payments. This will include all forms of transactions for example UPI, USSD, AEPS and RuPay Cards, but will exclude transactions through private credit cards and digital wallets.

In Digi-Dhan Vyapari Yojana for merchants weekly prizes worth Rs.50,000, Rs.5,000 and Rs.2,500. Mega draw on April 14 will have 3 mega prizes for consumers worth Rs.1 crore, Rs.50 lakh and Rs.25 lakh for digital transactions between November 8, 2016 and April 13, 2017. Three mega prizes for merchants worth Rs.50 lakh, Rs.25 lakh and Rs.12 lakh for digital transactions between November 8, 2016 and April 13, 2017 will be announced on April 14, 2017.

To ensure that the focus of the scheme is on small transactions (entered into by common people), incentives shall be restricted to transactions within the range of Rs.50 and Rs.3,000. All transactions between consumers and merchants; consumers and government agencies and all AEPS transactions will be considered for the incentive scheme.

The estimated expenditure on the first phase of the scheme (up to 14th April, 2017) is likely to be Rs.340 crore.

|

Digital Payment Challenges

The possibility of cybercrime, low-digital literacy and lack of infrastructure in the remote areas is the biggest challenge for digital payments in India.

Commenting about the challenges, Abhishek Rungta, CEO, Indus Net Technologies, said, “Improved infrastructure in terms of bandwidth quality and quantity, digital literacy, financial literacy, availability of payments software in vernacular and simple interface and security.”

Promoting digital literacy at the grassroots level, the Government is extensively using business correspondents and Gramin Dak Sevaks in the rural areas both to deliver and create an awareness.

The Government is asking telecom service providers to provide infrastructure for having internet facility on a continuous/permanent basis, without any disruption for making digital payments successful, especially in the suburban and rural areas. Besides it, there is a need to create good IT infrastructure for high-speed internet and fibre-based technology needs to be expedited.

Banks, mobile operators and mobile wallet companies should have a strong cybersecurity framework and should organize workshops etc to sensitize their customers about the digital transactions as well as the safety precautions to be followed in the case of digital transactions.

Speaking about PPP, Suneet Singh Tuli, President & CEO, DataWind, said, “Singapore, Sweden and Hong Kong are seen as the biggest 'standout countries’. India has a populace of more than 1.2 billion. However, there is still a considerable measure of potential for development in broadband use. There is immense capacity for innovation which needs to be worked upon for better performance. India needs to develop a world-class digital infrastructure through public-private partnership.”

Commenting on cybersecurity, Altaf Halde, Managing Director, Kaspersky Lab South Asia, said, “As part of Digital India, the Indian Government has already planned to launch ‘Botnet cleaning centres’. This proposal is part of the national cybersecurity policy to cleanup Botnet infections in Internet-enabled devices. Botnet is a network of malicious software that can remotely gain control of devices, steal information and carry out cyber-attacks like Distributed Denial-of-Service (DDoS) that prevent access of websites. This facility will be under the guidance of the national cybersecurity watchdog Indian Computer Emergency Response Team (CERT-IN).”

Speaking on cybersecurity, Shri Ravi Shankar Prasad, Minister of Electronics and IT and Law & Justice, Government of India, said, "To address concerns of cybersecurity, the Department will soon conduct a security drill both for the banks and NPCI. He urged the banks to adopt villages and promote digital inclusion and awareness about digital payments with them. He also requested that villages with majority tribal population be prioritized by banks for creating awareness on digital payments and transactions. This would be an opportunity for banks to become change agents to spread awareness about Digital India.”

In order to ease the digital payment operations at the level of merchants, UIDAI would shortly roll out the common Android-based Aadhaar-Enabled Payment System (AEPS) application developed in collaboration with TCS. In order to use this application for carrying out cashless transactions, merchants will need a smartphone and a fingerprint scanner. Transactions on this application can be done without any card or PIN. The application would be made available to all banks and the banks would encourage merchants in their vicinity to adopt this application.

Ratan P. Watal Committee on Digital Payment has suggested interoperability of the payments system between banks and non-banks, upgradation of the digital payment infrastructure and institutions and a framework to reward innovations and for leading efforts in enabling digital payments.

In its report, the committee has recommended that a medium-term strategy for accelerating growth of Digital Payment in India with a regulatory regime which is conducive to bridging the Digital divide by promoting competition, open access and interoperability in payments. The report recommends inclusion of financially and socially excluded groups and assimilation of emerging technologies in the market, while safeguarding security of digital transactions and providing a level-playing field to all stakeholders and new players who will enter this new transaction space.

All these initiatives will definitely help India in achieving $10 trillion by 2030.

Pravin Prashant pravin@varindia.com

See What’s Next in Tech With the Fast Forward Newsletter

for 2024 witnesses around 15,000 Indian participants")

Tweets From @varindiamag

Nothing to see here - yet

When they Tweet, their Tweets will show up here.