Indian market is one of the world’s fastest growing economies with US$2.2 trillion in GDP but still has more than 85 per cent of personal consumer expenditure made by cash. Despite its growing middle class and relatively strong cardholder base of 645M cardholders, debit and credit cards usage at point of sale (PoS)) is 1.7 transactions per cardholder in India.

A principal reason for slow progress towards greater adoption of electronic payments is the absence of available acceptance locations, preventing greater usage of and spending via cards. Currently, India has an approximate 2.7M point of sale devices,resulting in spotty and underdeveloped POS infrastructure coverage. Further, the acceptance network and volume that exists is concentrated in India’s primary cities, which account for an estimated 70 per cent of terminals and spend. The India Central Bank has indicated the country needs an approximate 20M POS devices to create a card acceptance infrastructure equal in size to other BRIC countries.

Overcoming barriers to developing acceptance is a key imperative for the country seeking to further expand electronic payments.Currently, an approximate 90 per cent of non-cash payments are processed through established card network infrastructures.At the heart of the traditional POS paymentacceptance networkis the interchange fee averaging between 0.75 per cent and 2.5 per cent —usually charged by a consumer’s bank to a merchant’s bank to facilitate a card transaction. The rate of electronic payment acceptance is low,as the high processing fee renders the value proposition non-compelling, especially for micro and small merchants, who form the bulk of India’s retail sector, and are the most important in serving low-income consumer segments.

AadhaarPay, biometric-enabled merchant payment acceptance solution,leveragesalternate clearing and settlement rails for person-to-merchant transactionsoriginating at the point of sale. Rather than ride on traditional card rails, Aadhaar Payleveragesthe real-time interbank network for transaction clearing and settlement.By disintermediating traditional interchanges and riding on less expensive bank rails, Aadhaar-based person to merchant payments lower processing fee and promote higher merchant uptake.The service uses Aadhaar, a unique national identity number issued by the Government to every citizen based on their biometric and demographic information, as a proxy for the customer’s bank account to facilitate transactions at the point of sale.

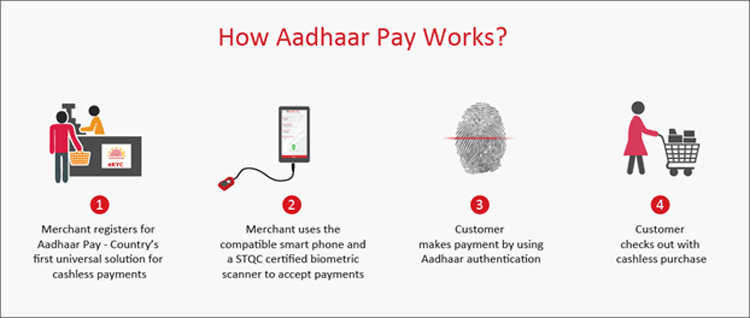

How it Works?

FSS Aadhaar Pay exploits three criticalelements -- bank accounts, mobility and digital identity -- to disrupt traditional POS business models. The service leverages the universal availability of the mobile device and Aadhaar -- India’s biometrically-enabled digital identity -- that covers 99 per cent of the population to advance the growth of digital payments. Envisaged as an open platform, the Unique Identification Authority of India (UIDAI Stack), allows payment service providers toconsumeAPIs, “on-demand” to authenticate customers.Besides leveraging Aadhaar for establishing user credentials, the national identity also serves as a financial address that can be directly linked to the customer’s bank account.

Any merchantwith a biometric reader and an Android phone can download the Aadhaar Pay application, self-register for the service using e-KYC, and start receiving payments. Customers make payments by scanning the fingerprint and entering the amount at the point-of-sale (PoS) terminal. Aadhaar Pay uses Aadhaar APIs to authenticate the customer’s biometric credentials mapped to the social security number. On successful authentication, the transactions are routed to the customer’s issuing bank. In contrast to setting-up a POS terminal, which takes between two and three weeks, FSS Aadhaar Pay takes a few minutes to set-up. Further, the cost of the POS is 80per cent lower than the cost of the conventional POS terminal.

Delivering a Multiplier Impact

Aadhaar Pay has a multiplier impact on the growth of the acceptancepayment ecosystem by bringing quick-to-deploy, mobile-based affordable POS infrastructure to merchantswhilstcreating a seamless transactional experience for customers.

Specifically, it triggers a virtuous cycle ofgrowth by:

Creating A Ready Market of 900 Million Captive Customers

Traditional acceptance networks need a large base of cardholders to be profitable. In emerging markets with a low base of carded users and unfamiliarity with digital payments, adoption remains slow. On the demand-side, Aadhaar Pay creates a ready addressable market of 900+ million customers by leveraging Aadhaar, as a primary transaction identifier. Customers can initiate payments using their fingerprint and Aadhaar number, eliminating hassles related to downloading multiple apps, swiping cards, remembering PIN/passwords, downloading e-wallets or carrying a phone.

Broadening the Merchant Ecosystem

On the acquirer side, Aadhaar Pay reshapes expensive acquirer distribution models by allowing banks to target previously under-penetrated micro-merchant segments with an efficient technology and commercial framework, easing the way for rapid onboarding and expansion of new acceptance points. The smallest street vendor, with the aid of a basic 2G phone and a fingerprint scanner device, can accept digital payments. To promote rapid uptake, there are no restrictions related to transaction amount, type of business, transaction volume, time, location, demography, and goods category

Offering a Low-Cost Solution

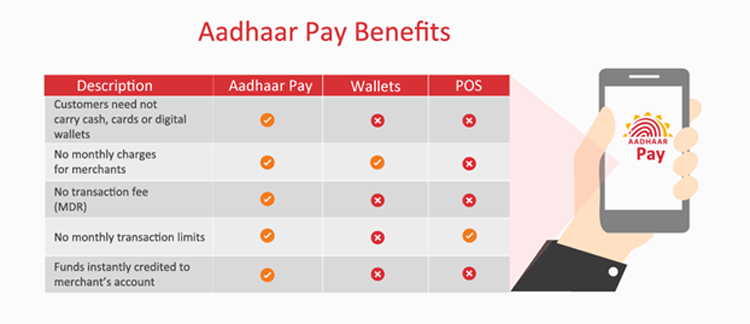

cost of a point-of-sale (POS) terminal in India ranges between INR 8,000 (USD 120) to INR 12,000 (USD 180); countervailing duties and taxes account for about 20 per cent of the price. In addition, the annual operating cost per terminal ranges between INR 3,000 (USD 45) and INR 4,000 (USD 60). FSS Aadhaar Pay mobile application, in comparison, can be downloaded online even on a 2G Android phone, connected to a biometric reader costing INR 2,000 (USD 30). The significant reduction in Capex and OPEX makes it an ideal solution for all merchant segments, especially micro-merchants with a small turnover and low transaction volumes.

Delivering DifferentiatedAdded Value Services

The “secret ingredient” to engineering the digital payments transformation is software. Hardware can be replicated easily, but software and services are much harder to copy, and this is where Aadhaar Pay brings a sustainable competitive advantage. Beyond the transaction, Aadhaar Pay potentially would takeon a more sophisticated, innovative approach to VAS. Merchants, big or small,could benefit from a complete packaged business solution, with the ability to customize specific components. This includes:

* support for QR codes

* ability to dynamically configure offers and discounts

* electronic invoices

* analytics and reporting: to sift through payment transactions and make recommendations to merchants for optimal inventory ordering or delivering offers to customers based on buying patterns and preferences.

* Settling Transactions in Real-Time

In the traditional interchange four-party payment models, settlement follows a typical T+1 cycle. Aadhaar Pay uses the bank account as a source of funds and all transactions are cleared and settled using the IMPS network (India’s real-time fund transfer network), ensuring immediate crediting of accounts, freeing funds and lowering working capital requirements for merchants.

Lowering Fraud Liability

As AadhaarPay leverages the bank account, it offers a low-risk product, with usage directly linked to the availability of funds in the customer’s account. For acquirers, there is no direct credit risk involved in transactions. This significantly lowers fraud liability and enables on-boarding of merchants traditionally deemed high-risk under the conventional acquiring models.

Whilst the service is in the initial rollout stages, AadhaarPay removes the multiple layers of friction that, merchants and customers encounter whilst making payments.For banks in India, who have recently opened Jan Dhan (no frills) accounts for the low-income demographic,a broad-based acceptance network would prevent instant encashment and improve the circulation of money in the digital format. Further, with the regulator waiving merchant fees, Aadhaar Pay would helpto develop sustainable acceptance that can enhance and fast-track the benefits of electronic payments.

Taking an early lead in the market,FSS launched Aadhaar Pay in April 2017. Currently, one of India’s top merchant acquirers, with an approximate 20 per cent share of the total POS market, has implemented Aadhaar Pay.

Suresh Rajagopalan

President Software Products, FSS

Tags: National ID, Universal Payment Acceptance, gdp, indian market, world's fastest growing economies, credit cards, India Central Bank, aadhar, aadhar card, Suresh Rajagopalan, President Software Products, FSS, varindia

See What’s Next in Tech With the Fast Forward Newsletter

Tweets From @varindiamag

Nothing to see here - yet

When they Tweet, their Tweets will show up here.