Breaking News

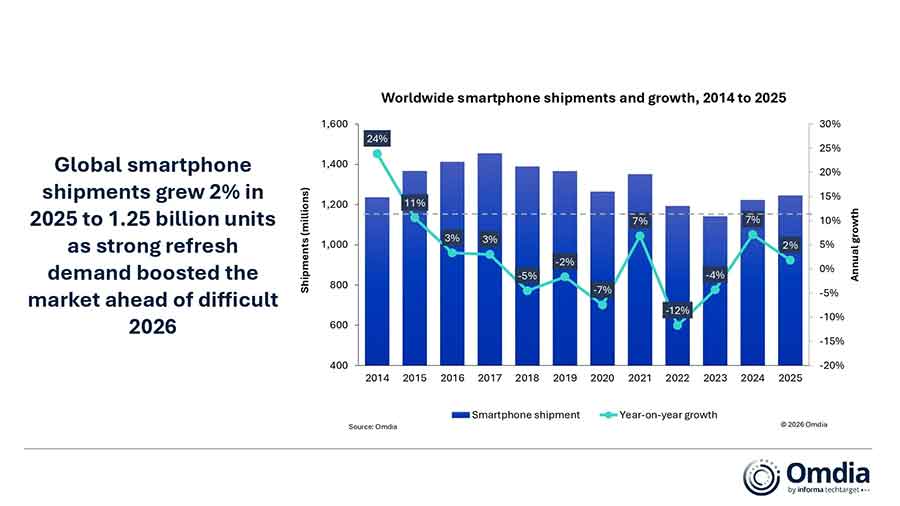

Global smartphone shipments rose 2% in 2025 to 1.25 billion units, marking the strongest annual performance since 2021, according to the latest research from Omdia. Growth was recorded across all regions except Greater China, which saw a marginal decline as the impact of government subsidies that supported early-2025 demand faded.

Omdia said steady demand from device upgrades and replacement purchases helped sustain momentum through the year, despite macroeconomic uncertainty. The market ended the fourth quarter of 2025 with 4% year-on-year growth, supported by seasonal demand and strong vendor execution. However, rising costs for key components, particularly memory, have begun to weigh on shipment expectations for early 2026.

Apple retained its position as the world’s largest smartphone vendor for the third consecutive year, delivering its highest-ever annual volume. iPhone shipments rose 7% to 240.6 million units in 2025, supported by a record-breaking fourth quarter. Apple also posted 26% year-on-year growth in Mainland China in 4Q25, driven by strong demand for the iPhone 17 series.

Omdia said steady demand from device upgrades and replacement purchases helped sustain momentum through the year, despite macroeconomic uncertainty. The market ended the fourth quarter of 2025 with 4% year-on-year growth, supported by seasonal demand and strong vendor execution. However, rising costs for key components, particularly memory, have begun to weigh on shipment expectations for early 2026.

Apple retained its position as the world’s largest smartphone vendor for the third consecutive year, delivering its highest-ever annual volume. iPhone shipments rose 7% to 240.6 million units in 2025, supported by a record-breaking fourth quarter. Apple also posted 26% year-on-year growth in Mainland China in 4Q25, driven by strong demand for the iPhone 17 series.

Samsung Electronics recorded a notable rebound after three years of decline, with shipments rising 7% year on year to finish marginally behind Apple. A strong fourth quarter, with shipments up 16%, reflected resilient flagship demand and a recovery in mass-market volumes. Samsung also regained share in entry-level and mid-range segments, reversing pressure seen in recent years.

Xiaomi defended its third-place ranking despite a challenging finish to the year, with shipments down 2% due to weakness in entry-level segments. The company continues to focus on value growth through portfolio expansion from POCO to premium devices and AIoT offerings. vivo climbed to fourth place for the first time, growing 4% to 105.3 million units, supported by strong performance in India and stable demand in its domestic market. OPPO completed the top five, with shipments of 100.7 million units, down 3% year on year, though it returned to growth in the fourth quarter.

Outside the top five, several vendors posted solid gains. Huawei regained the top position in Mainland China for the first time in five years, while HONOR and Lenovo achieved record volumes. Nothing emerged as the fastest-growing brand of 2025, with shipments rising 86% to exceed 3 million units.

Looking ahead, Omdia warned that supply-side pressures could challenge the market in 2026. “Escalating constraints in DRAM, NAND and other semiconductors threaten margins and pricing,” said Runar Bjorhovde, Senior Analyst at Omdia. He noted that smaller vendors with limited supplier leverage and high exposure to low-end devices would be particularly vulnerable.

Le Xuan Chiew, Research Manager at Omdia, added that vendors are likely to prioritise profitability and alternative revenue streams as market contraction becomes increasingly likely in 2026, making customer acquisition strategies and channel partnerships critical for long-term resilience.

See What’s Next in Tech With the Fast Forward Newsletter

Tweets From @varindiamag

Nothing to see here - yet

When they Tweet, their Tweets will show up here.